January, 2024

Cold Clarity

It’s time for a mind-clearing cold plunge.

While the numbers tell most of the story, I’ve sensed you are fatigued by the voice of the usual real estate soothsayers and gatekeepers: Toronto Regional Real Estate Board and The Bank of Canada.

TRREB based notes might be perceived as market-speak of a self-serving industry offering low lustre statistics and agents urging you to buy. The Bank of Canada’s persistent message is like a waddling grey character of Japanese anime – not too fast, not too slow, no discernable limbs but too many to count, the message: decisively indiscernible.

For a mind-clearing start to the year and a new voice let’s borrow from the reports (in italics) offered by National Bank of Canada Financial Markets – written by Daren King, Matthieu Arseneau and Jocelyn Paquet. As marketing documents and not a research report we are invited to share. The economists pull data from TRREB, so the information is in many ways the same, but it can be helpful to see it refracted through a different industry.

http://tinyurl.com/ymfcjftx (for the full reports) http://tinyurl.com/rfwfummy

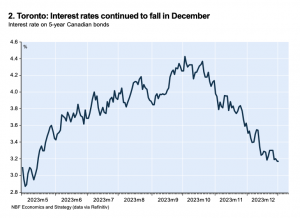

INTEREST RATES

For the third time in a row, the Bank of Canada decided to keep the policy rate unchanged in December but stated that the committee “is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed”.Why was the bank reluctant to signal that rate hikes are now a thing of the past, when inflation data is cooperating, and signs of a weakening economy are multiplying? Could it be that it didn’t want investors to get carried away by anticipating more rate cuts, leading to an easing of financial conditions in the long end of the yield curve that could stimulate growth?

We do not share these fears. Although the 5-year interest rate has fallen, it remains high, particularly in real terms. Overall, we expect the environment to remain difficult in 2024, as the economy has yet to feel the full effects of past rate hikes. We expect the Canadian economy to contract in the first half of the year, resulting in a decline of 0.2% for the year. Progress on the inflation front should enable the Bank of Canada to cut rates by 175 basis points in 2024 to give some breathing space to a faltering economy.

The Bank of Canada will announce its rate decision on January 24th at 9:30 am. Will they offer the first cut of the year?

SALES

Below, the bank analysts address the increase in sales in December. There is a factor affecting sales they did not mention and that is the newly implemented increase in Land Transfer Taxes. These took effect on January 1st. and apply to properties over $3M. In the Chestnut Park Real Estate Toronto office there was a surge in sales with some listings above $3M so buyers could get ahead of the increase. While these transactions may not have heavily impacted the entire board, they did impact purchasing in the core where most of you live.

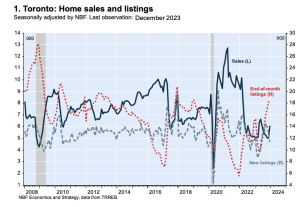

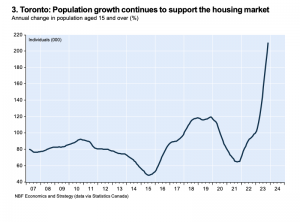

According to the Toronto Regional Real Estate Board (TRREB), seasonally adjusted home sales jumped 21.3% from November to December, a first increase in seven months that erased a good part of the decline recorded since spring (chart 1). This significant rise in sales has certainly been supported by the fall in bond yields, which have been pushing down fixed mortgage rates since October (chart 2), and strong demographic growth that remains unabated in the Canadian metropolis (chart 3)

The surge in sales in December hides a [very] different story depending on the type of property. We estimate that seasonally adjusted sales in the non-condo segment jumped 27.9% in the month, a second monthly increase in a row (chart 5). As a result, sales in that segment were at their highest level since April 2022.

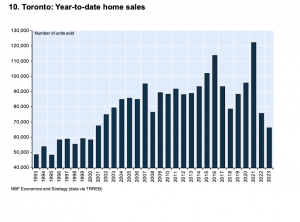

Simply put, interest rates are expected to go down. Buyers will come off the sidelines and look for their new homes. Chart #10 illustrates just how incredibly quiet the market has been. It rewinds us prior to 2001 for similar sleepiness, but with the anticipated clatter of the falling rates, buyers will wake up. Competition for desirable listings will increase. Sadly, there will be some stress sales as low covid mortgages mature.

Is it time for you to buy or sell? The answer to that is unique to your circumstance. Please get in touch if you want to talk it over: 416-925-9191.

jane@janedepencier.com